Partial Tax Exemption scheme

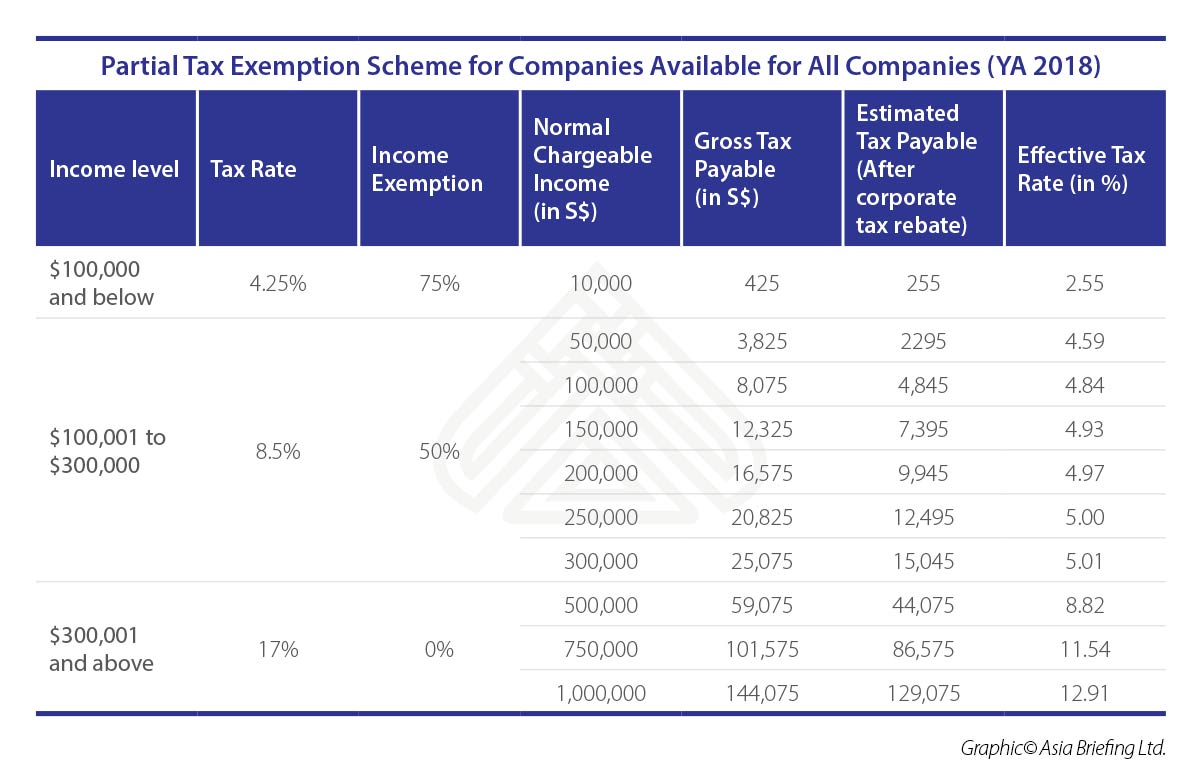

Companies that do not qualify for start-up exemption or are beyond the first three years of their incorporation, can avail for partial tax exemptions. This may amount to 75 percent tax exemption for the first S$10,000 (US$7,310) of normal taxable income and a 50 percent tax exemption on the next S$290,000 (US$212,017) of normal chargeable income. From YA 2010 to YA 2019, maximum exemption for each YA is S$152,500 (US$111,492).

Headquarters tax incentive

Companies with Regional Headquarters Award (RHA) and the International Headquarters Award (IHA) status pay a lower corporate tax rate of 15 percent on qualifying international income. Both RHA and IHA status are administered by the EDB.

Double tax agreements

Singapore has signed over 20 Free Trade Agreements (FTAs), and 74 comprehensive and 8 limited Avoidance of Double Tax Agreements (DTAs) that facilitate trans-border trade and make the cost of expanding overseas cheaper for Singapore-based firms. Accordingly, companies can claim a credit for the tax paid in the foreign country against the Singapore tax on eligible expenses, such as specified market expansion and investment development activities. This includes manpower expenses incurred when Singaporeans are deployed to overseas entities.

This text is part of a more complete analysis available for free.

Read the full article on ASEAN Briefing.